The cash cycle

How cash flows through your organisation

Unit 8

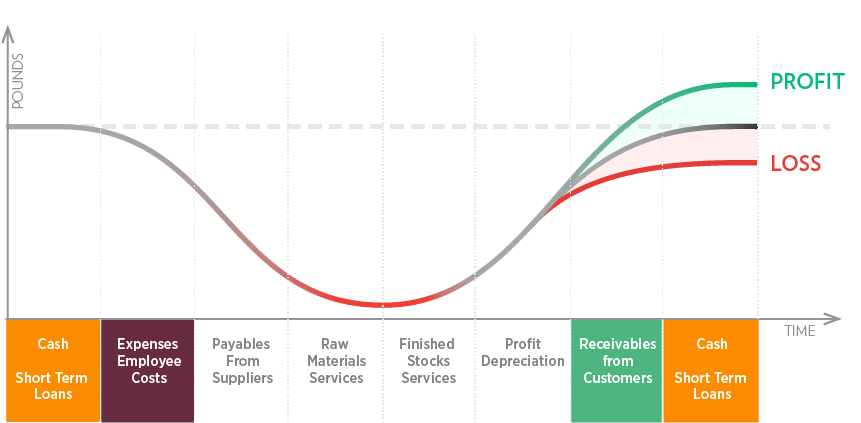

A vital part of successfully managing an enterprise’s financial position is an understanding of the cash cycle. In a sense cash flow is equivalent to the water in a central heating system delivering warmth to where it is needed, returning to the boiler to be reheated. Like water in the central heating system, cash in an enterprise is continuously circulating. The diagram shows the operating cash cycle.

The cash and short term loans provide a reservoir of cash, it is vital that this reservoir does not run dry.

This reservoir is made up of positive bank account balances,

physical cash plus any short term top-up facilities such as agreed overdraft facilities.

The main cash flow into the reservoir comes from amounts received from customers.

Outflows are mainly as payments to suppliers and employees and business operating expenses.

These outflows feed into products or services that are eventually sold to customers and the cycle starts again.

With each full cycle the amount in circulation is increased by the profit and depreciation, or decreased if there is a loss.

Note that the issue of depreciation is dealt with in unit 13.

The cash flows in the operating cash flow are usually known as working capital. Additionally non operating cash flows are important. The diagram is extended to show these items:

Clearly the payment of interest, tax and owners drawings or dividends can only come from the reservoir, as too can any repayment of borrowings and the purchases of fixed assets and investments. However if for the moment the reservoir is insufficient, then it can be topped from outside the operation of the business by the injection of new capital from the owners, taking out additional longer term borrowing and the sale of assets and investments if there are any.

An enterprise that does not have sufficient cash to pay its legitimate liabilities is said to have run out of liquidity.

It is a very serious financial situation and unless rectified quickly usually results in an enterprise failure.

Consequently a thorough understanding and management of the cash cycle is so significant to an enterprise.

LATEST NEWS

Bank reconciliation is the process of matching the balances in an entity's accounting records to the corresponding information on a bank statement. The goal is to ascertain that the amounts are consistent and accurate, identifying any discrepancies so that they can be resolved.

Understanding UK payroll is essential for businesses, self-employed individuals, and charities. It involves calculating and distributing wages, deducting taxes and contributions, and complying with HMRC regulations. Proper payroll management ensures timely, accurate employee compensation and adherence to tax and employment rules.

The Gift Aid scheme is well known in the charity sector and provides a welcome 25% boost to donation income. There is no limit to how often you can file your claim with HMRC so, if you have processes in place to be able to claim regularly.

Understanding the intricate details of the Church of England's parochial fees can be daunting. These fees, established by the General Synod and Parliament, cover a wide range of church-related services. Here's a deep dive into what these fees entail and how Liberty Accounts can streamline their accounting process for church treasurers.